Fundamentals and Valuation Check: Elevance Health Ahead of Upcoming Earnings

OVERVIEW

So, one of my biggest investments right now is Elevance Health. After dropping to fresh five-year lows not too long ago, the stock has bounced back nicely and is now trading in the $310 to $330 range.

Picture 1. Price performance of ELV 0.00%↑

As you probably know, the health insurance sector has been under heavy scrutiny recently - mainly because of uncertainty around ACA subsidies and other regulatory cuts.But interestingly, after that wave of pressure, some big players - including Berkshire Hathaway - were reported to be scooping up shares of certain insurers like UnitedHealth. Moves like that tend to lift sentiment across the board and can benefit the entire sector, Elevance included.

That’s why in this article, I want to take a closer look at Elevance’s most recent earnings report - to get a real sense of where the company stands today, and also to build a clearer picture ahead of their next earnings release, which is expected around October 15th to 18th.

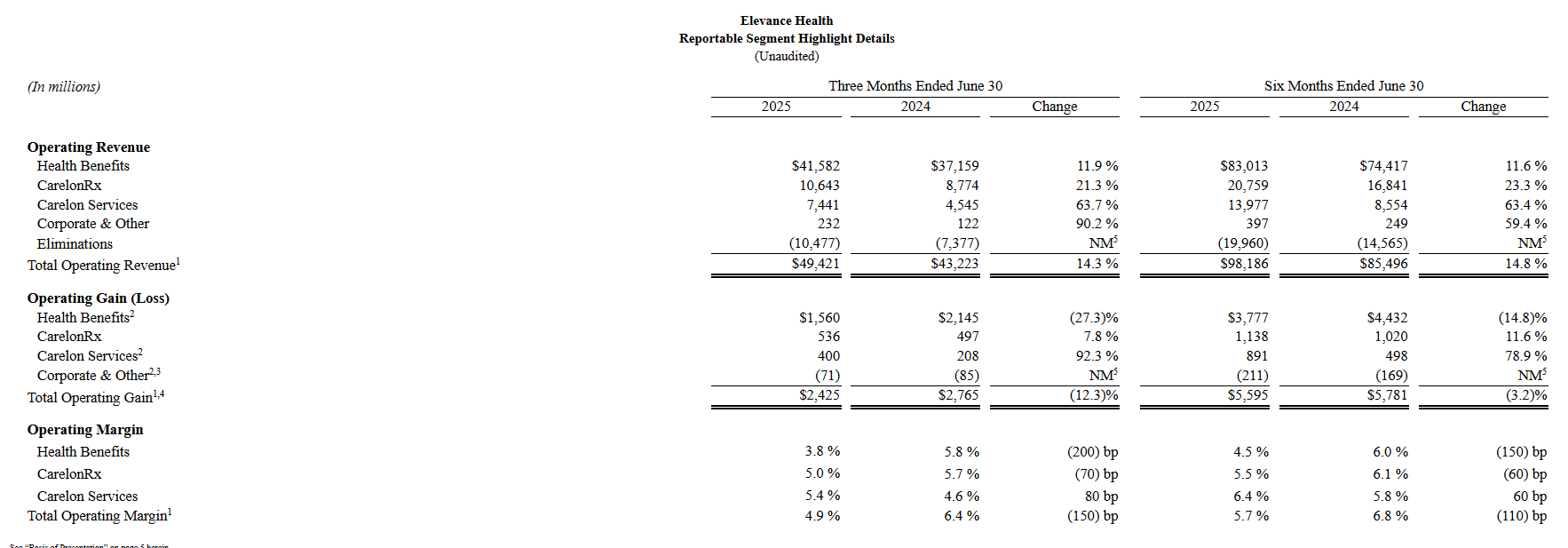

2Q EARNINGS REPORT

Elevance Health now expects 2025 GAAP net income per diluted share to be approximately $24.10 and adjusted net income per diluted share to be approximately $30.00. At the recent health care conference they reaffirmed its EPS guidance.

Picture 2. 2Q Earnings highlights

One notable takeaway from their latest earnings report is the ongoing pressure on operating margins. Over the past six months, margins declined by 110 basis points compared to the same period last year. Furthermore, during a recent healthcare conference, management acknowledged that they do not anticipate an improvement in the second half of the year, and benefit expenses will be elevated at ~90%. This indicates that margin headwinds are likely to persist, despite the initial growth in operating revenue.

MODELS & FUNDAMENTALS

Now that we have a clearer picture of the pressures the company is expected to face through the remainder of fiscal 2025, it’s worth stepping back and examining some key fundamentals.

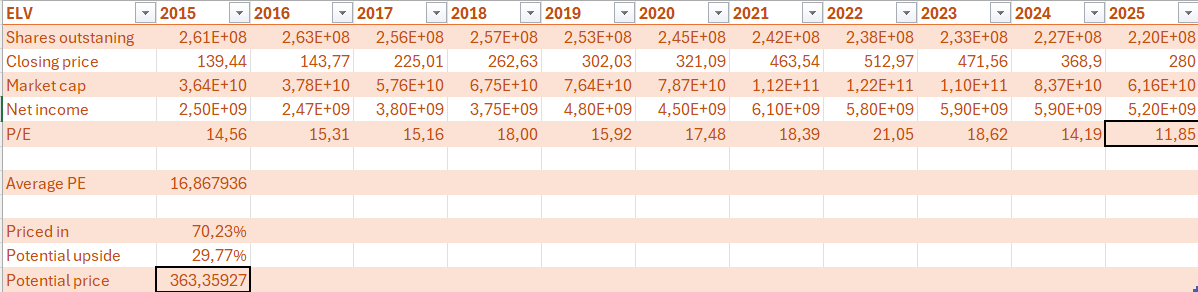

Looking at valuation, Elevance has traded at an average P/E ratio of 16.86 over the past decade. If we apply that historical multiple to the company’s recent low of $280 per share, it implies a potential upside of roughly 30%, pointing to a theoretical fair value of around $363.

Picture 3. P/E model

Next, considering the price-to-sales ratio, the picture appears similar. At recent lows, Elevance was trading at a multiple of just 0.33, compared to its historical average of 0.64. This gap suggests an upside potential of nearly 50% from those depressed levels, should the valuation revert closer to its long-term norm.

Picture 4. P/S model

Lastly, when we look at the price-to-operating income ratio, the 10-year average stands at 9.88. Applying this multiple to the company’s recent low suggests a potential upside of about 28%, implying a fair theoretical value of at least $359 per share.

Picture 5. P/OI model

Bringing these valuation measures together, the average of the three approaches points to a theoretical fair value of around $380 per share. From the recent lows, that would imply an upside of roughly 26%. Even from the current level of $320 per share, there remains about 16% potential upside. Technically, such a move would also align with a reclaim of the 200-day EMA, which could open the door for further gains if that level is successfully held as support.

Another factor that adds to Elevance’s attractiveness is its consistent capital return policy. The company continues to pay a regular dividend, which stood at $1.71 per share in the second quarter. In addition, Elevance repurchased 0.9 million shares during the latest quarter at a weighted average price of $410. These initiatives highlight management’s commitment to returning value to shareholders through dividends and buybacks, independent of the stock’s price performance.

CONCLUSION

To sum up, from a technical standpoint, the company has rebounded about 17% from its recent lows, driven largely by strong institutional interest. Margin pressures - primarily tied to elevated benefit expenses - remain a headwind, meaning further upside will depend on Elevance’s ability to adapt to these conditions and, potentially, on additional government support. Valuation models still point to remaining upside, while buybacks and dividends add an extra layer of attractiveness for investors. Macro pressures could weigh on the stock in the short term, but in my view, the long-term outlook remains positive. Healthcare has always been, and will continue to be, one of the cornerstones of human society - even if most of us only begin to appreciate its value when it becomes personally necessary.

Enjoyed this read?

Check more of my work:

Socials: X - Financial Pulse

Website: Financial Pulse